When we talk about economic levers, there's one in particular that the Reserve Bank of Australia (RBA) keeps a firm grip on: the official cash rate. But before we dive into interest rates, it's worth understanding who the RBA is and what it actually does.

The Reserve Bank of Australia is the nation's central bank. Its job is to help keep our economy running smoothly. That means managing inflation, promoting stable employment, and supporting economic growth. One of the main ways it does this is by adjusting the cash rate—a key interest rate that influences how much it costs to borrow or save money across the country.

You've probably heard the RBA mentioned on the news during interest rate announcements, but its decisions go far beyond headlines. They affect everything from mortgage repayments to grocery bills and job opportunities. So whether you're studying Economics in Year 12—through HSC, VCE, QCE, WACE, SACE, or IB—the Reserve Bank of Australia and its monetary policy decisions are core curriculum topics.

This blog unpacks how interest rates are set, why they change, and how this connects to key learning outcomes across Australia's senior economics courses.

Current Cash Rate: 3.85%

Latest Move: Increase of 0.25% (February 2026)

After a year of relief in 2025 where rates were cut three times to stimulate the economy, the RBA has kicked off 2026 with a rate hike. This highlights just how tricky it is to keep inflation in the "target band" of 2–3%.

What is the Cash Rate, and Why Should We Care?

The cash rate is the interest rate on overnight loans between banks. While that sounds like it only affects big institutions, it actually influences the entire economy. Banks use it as a benchmark to set interest rates for loans, credit cards, and savings accounts.

In short: when the RBA changes the cash rate, it creates ripple effects that affect your wallet, your job prospects, and the broader economy.

The RBA adjusts the cash rate to maintain a balance between economic growth, inflation, and employment. These changes are part of the RBA's broader mandate: to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of Australians.

The “Why” Behind Interest Rate Changes

Here's a simple way to understand it:

- When inflation is too high (like in 2022–2023 and early 2026): The RBA raises interest rates to "cool" spending. Higher rates make borrowing expensive and saving attractive, which reduces demand for goods and services.

- When growth is slow (like in 2020 or 2025): The RBA lowers interest rates to "stimulate" the economy. Cheaper loans encourage businesses to invest and households to spend.

This push and pull is part of a broader strategy called monetary policy—a major piece of Australia's macroeconomic puzzle.

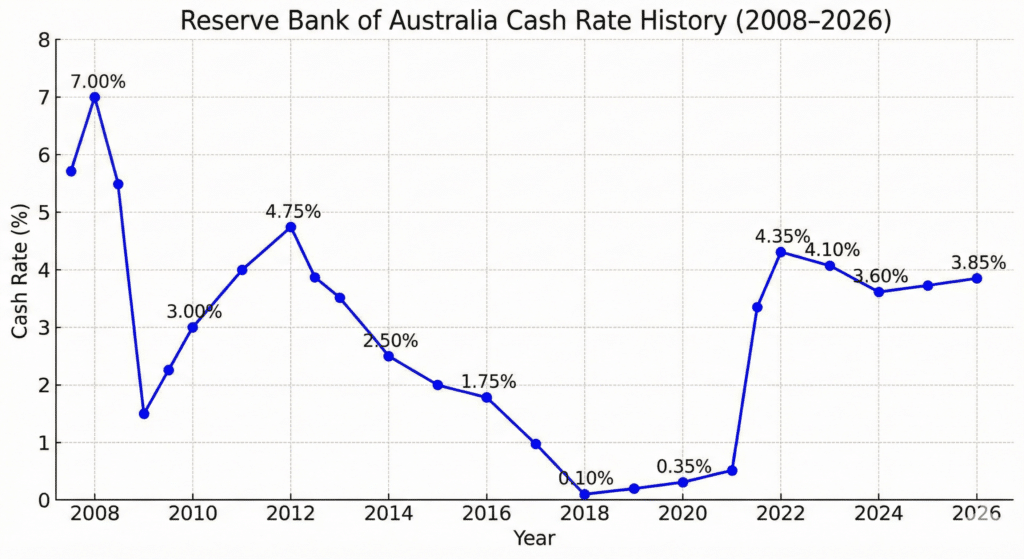

A Timeline of RBA Cash Rate Decisions (2008–2026)

Here's a breakdown of the key eras that have shaped the economic landscape in Australia since 2008, including the recent "U-turn" in 2026.

| Date | Cash Rate | Explanation |

|---|---|---|

| September 2008 | 7.00% → 6.75% | The Global Financial Crisis (GFC) hit. The RBA cut rates aggressively to prevent a recession. |

| April 2009 | 3.00% | Rates were slashed aggressively as the full impact of the GFC hit. The aim was to keep businesses afloat and Australians in jobs. |

| November 2010 | 4.75% | Australia was recovering steadily. The RBA cautiously raised rates to manage growth and prevent overheating. |

| August 2013 | 2.50% | With the mining boom cooling off and global growth slowing, the RBA eased the cash rate again to stimulate domestic demand. |

| May 2016 | 1.75% | Inflation remained below target, prompting another cut to support consumer spending and business activity. |

| March 2020 | 0.50% | COVID-19 struck. The RBA made rapid and sharp rate cuts to buffer the economy from the worst impacts of lockdowns. |

| November 2020 | 0.10% | COVID-19 Pandemic. The lowest rate in history was set to support the economy during lockdowns. |

| May 2022 | 0.35% | The Inflation Spike. Supply chain issues and global stimulus caused prices to soar, forcing the first hike in a decade. |

| June 2023 | 4.10% | After a series of increases, the rate hit a peak as the RBA worked to contain inflation while balancing economic momentum. |

| November 2023 | 4.35% | After 13 rapid hikes, the rate peaked at 4.35% to crush inflation, staying there for all of 2024. |

| February 2025 | 4.10% | The Easing Cycle Begins. With inflation falling, the RBA cut rates for the first time in 4 years to help households. |

| August 2025 | 3.60% | |

| February 2026 | 3.85% | The Rebound. Inflation proved "sticky" (rising back to 3.8%), forcing the RBA to reverse course and hike rates again. |

Visualising the Journey

RBA’s cash rate history from 2008 to 2026:

Where This Fits In Year 12 Economics

Understanding the RBA’s recent pivot in 2026 is gold for your exam responses. It demonstrates the lag effect and the difficulty of "fine-tuning" the economy.

- HSC Economics (NSW): Use the 2026 hike to discuss the conflict between economic objectives (fighting inflation vs. supporting growth).

- VCE Economics (Victoria): Analyse the transmission mechanism. Why did the 2025 cuts increase demand so quickly that inflation came back?

- QCE Economics (Queensland): Focus on price stability. Why did the RBA act so quickly in Feb 2026 when inflation hit 3.8%? (Hint: The target is 2–3%).

If you’re preparing for your exams, RBA decisions and their justifications are often used in multiple-choice, short-answer, and extended responses. Knowing how to apply this knowledge to real-world examples like the GFC or COVID-19 gives you a critical edge.

Why This Matters to You

Even as a student, these shifts impact your life:

- Part-time jobs: When rates go up (like now), businesses often tighten budgets, which can mean fewer shifts for casual staff.

- Cost of Living: The RBA hiked rates because prices (inflation) were rising too fast. The goal is to make your lunch and transport cheaper in the long run, even if it hurts borrowers now.

- HECS/HELP: Indexation of student loans is tied to inflation. High inflation means higher student debt growth, so the RBA's fight is actually helping your future self.

Final Thoughts

The decision to raise rates in February 2026 after a year of cuts serves as a reminder: the economy is unpredictable. The RBA doesn't just "set and forget." They are constantly watching the data—like the recent spike in electricity prices—and adjusting the levers to keep Australia on track.

If you can explain why the RBA had to reverse course in 2026 in your essays, you’ll demonstrate a high-level understanding of contemporary economics.

If you found these tips helpful, you a reach out to an Economics tutor on Learnmate for further support this year.

Glossary of terms

| Term | Definition |

|---|---|

| Cash rate | The interest rate set by the RBA for overnight loans between banks. It influences all other interest rates in the economy. |

| Inflation | The general increase in prices over time. A small amount of inflation is healthy, but too much can erode purchasing power. |

| Monetary policy | The actions taken by the RBA (mainly interest rate changes) to influence the economy’s performance. |

| Global Financial Crisis (GFC) | A major worldwide economic downturn that began in 2008, triggered by the collapse of financial institutions in the US. |

| Economic stimulus | Government or central bank actions (like interest rate cuts) designed to boost economic activity during slowdowns. |

| Overheating | When the economy grows too quickly, leading to inflation and unsustainable bubbles. |

| Tightening cycle | A series of interest rate increases used to cool the economy and control inflation. |

| HECS/HELP | Australia’s student loan system, which adjusts repayments based on income and inflation. |